ARK Overview

ARK Investment Management LLC (ARK or ARK Invest) was founded in January of 2014 by CEO and CIO Cathie Woods. ARK Invest was founded with the intent of capitalizing on investments by focusing on companies that revolve around ‘disruptive innovation’. ARK is an acronym for Active Research Knowledge. ARK takes a thematic approach towards the investment process where they seek to capitalize on long-term trends that can better adjust for rapid and future change and overall long-term value creation. ARK’s thesis for future innovation and change revolves around the following 5 Principles and Platforms for what they believe is ‘Disruptive Innovation’:

1) Artificial Intelligence

2) Blockchain Technology

3) DNA Sequencing

4) Energy Storage

5) Robotics

These 5 Platforms are encompassed and represented through ARK’s 5 ETFs

- ARKK (ARK Innovation ETF)- Focuses on Artificial Intelligence, Autonomous Vehicles, Fintech, DNA Sequencing, Robotics, and 3D Printing

- ARKQ (Autonomous Technology & Robotics ETF)- Focuses on Autonomous Transportation, Robotics and Automation, 3D Printing, Energy Storage, and Space Exploration

- ARKW (Next Generation Internet ETF)- Focuses on Cloud Computing & Cyber Security, E-Commerce, Big Data & Artificial Intelligence (AI), Mobile Technology and Internet of Things (IoT), Social Platforms, and Blockchain & P2P.

- ARKG (Genomic Revolution ETF)- Focuses on Targeted Therapeutics, Bioinformatics, Molecular Diagnostics, Stem Cells, Agricultural Biology.

- ARKF (Fintech Innovation ETF)- Focuses on Transaction Innovations, Blockchain Technology, Risk Transformation, Frictionless Funding Platforms, Customer Facing Platforms, New Intermediaries.

General Notes:

- ARK Invest publishes its quarterly results, new findings, and general research on its website

- ARK Invest posts a summary of its trades and transactions across all of its ETFs at the end of each day.

- ARK’s investment horizon is a minimum of 5 years.

- ARK’s minimum requirement to be in the portfolio is to have a compound annual return of 15%. (A doubling over 5 years.)

Investing in the Future

Through the lens of investing, company innovation is the act of changing the way the world works and creating a more sustainable future through vertical progress. Vertical progression is defined as doing or creating new things and or implementing strategies that help scale a product or service inside an existing market. As mentioned earlier, the Firm was founded in 2014 to focus on disruptive innovation because they believed there was an unmet need for innovation in the public markets post 2000 Telecomm Bust and 2008 recession. Post-recession, the ARK team saw risk aversion rise in the market which meant individual investors started shifting their mindset and investing their capital in more passive and ‘safer’ strategies ie) Index Funds, Mutual funds, ETF’s, etc.

This shift in the search for innovation moved more towards the private markets primarily to Private Equity and Venture Capital, which shifted all the attention away from innovative companies in the public sector. As a result, there were enormous miscalculations and mostly misevaluations of companies that were primed to perform well in public markets post IPO, etc. These public companies were neglected by private market investors naturally and glossed over by index funds filled with incumbent companies. To iterate further, in the past decade or so, Silicon Valley has veered further and further away from public markets with the influx of capital and successful venture dollars being put to use towards private markets to fuel start-ups and the next generation of public companies. One of the more notable requirements to be in the S&P 500, a stock market index that measures the performance of 500 large companies listed on the exchange, a company has to have at least 50% of its shares available for public trading and a market capitalization of at least ~$8 Billion. This is where the disposition lies.

Conceptually, Indexes such as the S&P 500 are backwards-looking because the companies in the portfolio are there based on the metrics and growth that occurred in the past 10–20 years. This ultimately means that newer innovative public companies that are extremely fast-growing are far too early in their maturation cycle to be in indexes despite their exponential growth. Incumbent companies that have been in these indexes for years represent a huge misallocation of capital as more than 50% of stock ownership and capital in the U.S are held in passive strategies and investments. Not to say passive strategies or passive investing is poor judgment; however, these passive vehicles are ignoring the low-hanging fruit and new wave of companies and technologies as the grounds are shifting beneath retail investors with new entrants and disruptive companies becoming exponentially more pervasive in the public markets and everyday life. A handful of the companies in ARK’s ETFs are not in Index funds because they are far too early in their maturation cycle and are not yet considered incumbent players with a 20–30 year track record that would be in traditional indices.

Decades ago, companies that are currently in indexes use to be considered ‘cutting edge’. These incumbent companies were technically considered the ‘new entrants’ in the market and disruptive in their own respect given the respective time frame. However, now that technologies are constantly evolving and accelerating over time, new entrants are beginning to emerge and surface around every corner. Naturally, the incumbents in indexes are in search of a way to continue to innovate and keep up with new entrants and market disruptors. Typically when incumbents get disrupted and new entrants replace them, they tend to get more valuable. This mental model applies not only to companies but to other facets of life as well. The irony we find in traditional benchmark indexes is that their returns have been subpar and ‘average’ year over year because the innovation and high growth companies are not being put in their indexes because they are currently full of market incumbents.

Circling back to ARK Invest, ARK’s goal is to capitalize and take advantage of this market inefficiency by investing in this clear and obvious arbitrage opportunity. Not only does ARK invest in their thesis of what they believe is the future of innovation, but they also are long-term thinking with their approach to investing in the future. The Firm focuses on a minimum of a 3–5 year window of investments and also serves as a general liquidity provider in the market for these companies. For a stock to be considered as a part of the portfolio, the research team must conclude that the upside and trajectory of the stock must have a compound annual return of 15% or a doubling in over 5 years. Typically, if a company or stock plummets due to short-term thinking or massive sell-off from an event such as poor quarterly results, ARK will pick up the stock, capitalize, and invest in the underpriced stock. Vice-versa, if a company is outperforming, the Firm will turn to general asset allocation and re-balance their portfolio as their ETFs do not allow any stock holdings to have more than a 10% weight in their ETFs for tax purposes. ARK Invest can be regarded as the closest thing to a Venture Capital Firm in the public markets from investing in a high growth standpoint.

Why Now?

Contrary to common belief, a recession and or market downturn actually accelerates the shift to innovation and adaptation to new processes and technologies. New technologies and new processes are adapted due to the nature that consumers and companies both are scared and are willing to change the way they choose to do things and operate as their backs are against the wall.

A recent example being the shift to remote work with Zoom and a myriad of other work applications being heavily relied upon and adapted during this pandemic. This pandemic has proven that proximity and location to a physical office have nearly been muted in a remote world as processes and efficiencies of remote work have far outperformed expectations. With that being said, more and more companies in Silicon Valley are unsure whether or not they will continue to have the 5 day work week in the office given general convenience and frictionless ease for their employees. This rationale has also been reinforced by recently strong quarterly results and work metrics for many companies. If anything, the silver lining in the pandemic is that it has proven how efficient employees can be working remotely and how the location of a person is not a core tenant or function in assessing whether or not real work can be done.

Given the relevant case study of the pandemic, it has been found that innovation gains market share at an accelerated rate in a crisis or pandemic because applications are better, cheaper, faster, much more efficient, productive, and heavily relied upon for solving problems. Adaptation of new technologies equates to an acceleration in productivity growth. As a result, innovation steals market share during a market downturn. Ex) The Technology sector Post Q2 Covid-19 results from Q3 2020 to present-day Q1 2021.

It has been apparent that markets are currently at an all-time high with new highs being recorded week over week for the past quarter. The common lexicon that is pervasive and commonly synonymous with Silicon Valley is that technology, more specifically Cloud computing and Open Source to name a few, have outperformed better than other categories this year. This is valid to an extent as the technology sector has appreciated ~28% YTD in 2020 with the other sectors appreciating approximately on average at 4% (current as of 9/30/2020). Despite all-time highs, people remain extremely bullish on investing in ARK’s positions based on the premise that these holdings will be a minimum of a 3–5 year investment or a lock-up for that matter, some of which people would expect to hold for 10+ years.

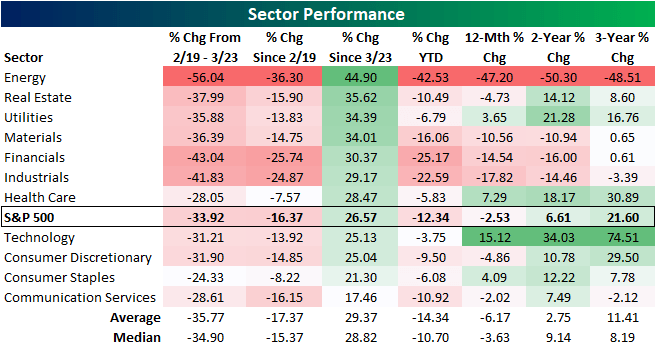

Summary of Sector Performance the past several years:

Obviously, there is a huge emotional component to investing where markets ebb and flow year over year, quarter over quarter, or whatever the time horizon you’d like to imagine. However, at its core, disciplined investing is blocking out the outside noise and letting the companies take their toll and ride. Over a 3,5,10, 20-year horizon, companies will continue to grow at an exponential rate, specifically in the technology sector as we find that technology is starting to permeate through other sectors such as energy, healthcare, industrial, financials, etc. Technology is not replacing these industries, rather they serve as accelerators for all these industries and help empower them. Ultimately, successful companies are veering towards becoming tech companies or companies that heavily rely on strong technological processes or infrastructures.

What I’ve learned from the past several years in public markets is that you make all your money on companies or holdings that can run. In the past, people have been extremely hesitant to put money into certain stocks because pricing seemed way too high and aggressive at the time. In general, I’d say most of the time those are usually mistakes. You make the majority of your money based on your top winners. Ultimately there is almost no price too high to pay relative to where outcomes can be. Psychologically, it’s really hard for us to forecast and imagine how large outcomes can actually be. The biggest problem is not understanding or visualizing how big companies can be and their true upside and potential.